If you haven’t checked your credit report recently, you’re not alone. But let me tell you--waiting until there’s a problem is one of the costliest financial mistakes you can make.

Your credit report doesn’t just affect your ability to get a loan—it impacts your interest rates, your insurance premiums, your ability to rent an apartment, and even some job opportunities. It’s a mirror of your financial identity. The question is: What is yours really saying about you? Let me share two real client stories that show why checking your credit report regularly isn’t just smart—it’s essential. 🧾 Case Study 1: David – Denied Over a $123 CollectionDavid was ready to buy his first investment property. He had the income, the savings, and the motivation. But when his mortgage pre-approval came back denied, he was blindsided. A $123 utility bill—sent to an old address—had gone to collections without his knowledge. It dropped his score by nearly 70 points. “I had no idea it even existed. If I had checked my credit, I could’ve handled it months ago,” he told me. ✅ What we did: At REI Invest Capital Loan Credit Repair, we helped David dispute the account, provide a change-of-address history, and request deletion. Within 30 days, the collection was removed, his score recovered, and he successfully closed on his property. 🔍 Case Study 2: Shanelle – Identity Theft Caught Just in TimeShanelle had worked hard to clean up her finances. So when she got a “thank you” letter for a credit card she never applied for, she immediately pulled her credit report. Two new hard inquiries and a fraudulent credit card had already appeared. “If I hadn’t caught it when I did, it could’ve ruined everything I’ve worked for,” she said. ✅ What we did: We helped her freeze her credit, file an FTC Identity Theft Report, and dispute the fraudulent account. The account was removed before it was ever used, protecting her credit and hard-earned progress. 💡 Why Regular Credit Checks Are So ImportantHere’s what most people don’t realize: your credit report updates every month. One mistake or unauthorized account can set you back significantly—unless you catch it early. Checking your credit report regularly helps you:

✅ 3 Smart Habits to Start Now1. Check your report every 3–4 months. Rotate through the three bureaus at AnnualCreditReport.com to stay on top of changes year-round. 2. Dispute inaccuracies immediately. Late payments, duplicate accounts, and wrong limits can hurt your score. Don’t ignore them. 3. Read the full report—not just the score. Apps are helpful, but only the full report shows what lenders actually see. 📞 Let’s Go Through Your Credit Report—TogetherIf it’s been a while since you looked at your report, or if something feels off, I invite you to sit down with me or someone from our team. At REI Invest Capital Loan Credit Repair, we offer a free 30-minute credit consultation where we will:

📅 Schedule online here: 📞 Or call us directly at (312) 626-0116 to book your spot. Don’t wait until there’s a problem to check your credit. Check it now—fix what’s wrong—and protect your financial future. Let’s take the guesswork out of your credit report, one line at a time. Top 5 Mistakes Hiding in Your Credit Report (And How to Fix Them) Your credit report is more than just a number—it’s a roadmap of your financial trustworthiness. Yet, according to the Federal Trade Commission (FTC), one in five Americans has a credit report error significant enough to affect their score. These errors can lead to loan rejections, higher interest rates, denied apartment applications, or even lost job opportunities.

The good news? You have the right to review, dispute, and correct inaccuracies—but only if you know what to look for. Below, we reveal the top five mistakes that might be hiding in your credit report and show you exactly how to fix them before they cost you thousands. 🔎 Mistake #1: Accounts That Don’t Belong to You What It Is: One of the most damaging and common mistakes is the inclusion of accounts that you never opened. These may be due to:

These accounts may show missed payments, high balances, or collections—seriously hurting your score. ✅ How to Fix It:

🔍 Mistake #2: Incorrect Payment Status or History What It Is:Payment history makes up 35% of your FICO score, so errors in this area are especially damaging. A single late payment incorrectly reported as “missed” can drop your score by 50–100 points. ✅ How to Fix It:

📊 Mistake #3: Duplicate Accounts or Debts What It Is:Sometimes the same debt is reported more than once under different names or account numbers. This can inflate your total debt and distort your credit utilization ratio. ✅ How to Fix It:

🧾 Mistake #4: Outdated Negative Information What It Is:Negative items such as collections, charge-offs, and bankruptcies are only allowed to stay on your credit report for a certain period:

✅ How to Fix It:

📉 Mistake #5: Incorrect Credit Limits or Balances What It Is: Credit utilization—how much credit you’re using compared to your total limit—makes up 30% of your score. If a creditor reports a lower limit than what you actually have, your utilization may appear much higher than it is. ✅ How to Fix It:

🛠️ The Bottom Line: Monitor, Dispute, and Protect Your credit report is not just a record—it’s a reflection of your financial reputation. By checking your reports regularly, spotting errors, and taking action quickly, you can protect your credit score and open doors to better financing, housing, and employment opportunities. 📅 Need Help Fixing Credit Report Errors? Book a Free Consultation If you’ve spotted errors or just want an expert set of eyes on your credit report, REI Invest Capital Loan Credit Repair is here to help. Our team will:

🕒 Schedule your FREE 30-minute consultation today and get your credit report back on track. 👉 Book Now Your credit is your currency—make sure it’s accurate, updated, and working for you. Let REI Invest Capital help you fix what’s broken and build what’s next.  How to Read Your Credit Report Like a Pro?Your credit report plays a powerful role in your financial life. It can determine whether you're approved for a home loan, a car lease, a business credit line—or denied. But while most people check their credit score occasionally, few know how to actually read and interpret their full credit report.

Understanding what’s on your report—and how to read it like a pro—is essential for protecting your credit, catching costly errors, and making smart financial moves. Whether you're rebuilding after a hardship or preparing for a major purchase, here’s what you need to know about decoding your report and taking control of your credit health. 📄 What’s Inside a Credit Report? Your credit report is a detailed snapshot of your borrowing history, compiled by one or more of the three major credit bureaus: Experian, Equifax, and TransUnion. These reports are used by lenders, insurers, landlords, and even employers to evaluate your financial reliability. Each report includes:

🔍 How to Read Your Credit Report Like a Pro 1. Start with Your Personal Information Double-check that your name, addresses, Social Security number, and employment history are accurate. Even minor mistakes can lead to confusion or misreporting. 2. Review Every Account Carefully Each account lists the creditor, account type, balance, credit limit, payment history, and status. Look out for:

3. Pay Close Attention to Payment History This section is critical—it tells lenders how reliably you’ve paid your debts. Even one missed payment can negatively impact your score. ✅ Green marks mean on-time payments ⚠️ Yellow or red marks signal delinquencies 4. Monitor Credit Utilization Your utilization ratio shows how much of your available credit you're using. Ideally, keep it below 30%—under 10% for the best scores. Example: If you have a $5,000 credit limit and a $4,500 balance, that’s 90% utilization—much too high. 5. Review Collections and Public Records Collections and court judgments stay on your report for years. Even if you’ve paid them off, they could still show as negative unless updated. Make sure:

6. Understand the Inquiries Section Your report distinguishes between hard inquiries (which can affect your score) and soft inquiries (which do not). 🔍 Too many hard inquiries in a short time can make you look risky to lenders. 🛑 Common Credit Report Mistakes to Watch For

These errors are more common than you think—and they can unfairly drag down your credit score if left uncorrected. 📉 What to Do If You Spot an Error You have the legal right to dispute inaccurate items directly with each credit bureau. However, understanding the proper documentation, strategy, and timelines can be challenging on your own. That’s why many turn to professional credit repair experts who know how to navigate the system, communicate with bureaus, and get results quickly. ✅ Schedule a 30-Minute Credit Repair Consultation Today If you’re unsure what to look for on your credit report, or you’re ready to clean it up and start building toward better financial opportunities--we’re here to help. At REI Invest Capital Loan Credit Repair, we’ll help you:

📅 Click below to schedule your FREE 30-minute Credit Repair Consultation now. Let’s take the guesswork out of your credit and set you up for financial success. 👉 Book Your Consultation Now  When it comes to applying for a mortgage, auto loan, or business financing, most consumers assume their credit score is the only thing that matters. But industry insiders reveal that lenders dig much deeper than just three digits. They’re analyzing patterns, payment behaviors, and red flags buried within your credit report.

With interest rates fluctuating and lending standards tightening in 2025, experts say understanding how to present a strong credit profile is more important than ever. Whether you're rebuilding after hardship or aiming for top-tier approval, here’s what lenders are really looking for—and ten actionable strategies that can help boost your score fast. What Lenders Examine Beyond the Score? According to financial analysts, lenders use your credit report to gauge your risk as a borrower. "They’re not just looking for a high score," says Angela Ross, a senior underwriter at Midwest Lending Group. "They want to see stability, consistency, and responsible credit use." Key factors include:

10 Tips and Tricks to Boost Your Credit Score and Improve Lender Approval Odds 1. Prioritize On-Time Payments - Late payments can drop your score dramatically. Set up auto-pay or calendar reminders to stay on track. 💬 “One 30-day late payment can drop a good score by over 90 points,” says credit specialist Dana Williams of REI Invest Capital. 2. Lower Your Credit Utilization Ratio - Keep balances below 30% of your total credit limit. The lower, the better. 💡 Requesting a credit limit increase can improve utilization without additional spending. 3. Don’t Close Old Accounts - Old accounts contribute to your credit age. Closing them can shorten your history and hurt your score. 4. Add Authorized User Tradelines - Becoming an authorized user on someone else’s well-managed credit card can boost your score instantly. 🔍 REI Invest Capital offers tradelines that can add years of history and higher limits to your report. 5. Monitor Your Report for Errors - Incorrect data, outdated accounts, and duplicate entries can unfairly drag your score down. Check your report at least once a year via AnnualCreditReport.com. 6. Avoid Frequent Credit Applications - Each hard inquiry can reduce your score slightly. Space out applications and avoid applying for unnecessary credit. 7. Pay Down Balances Before Statement Dates - Most creditors report your balance on the statement closing date, not the due date. Paying early can lower what’s reported. 8. Use Tools Like Experian Boost - Services like Experian Boost or rental reporting platforms let you add utility and rent payments to your report. 9. Diversify Your Credit Mix - A healthy combination of installment loans and credit cards shows lenders you're capable of managing different types of debt. 10. Be Cautious About Co-Signing - Co-signing means you're legally responsible for another person's debt. Missed payments affect your report too. The Bottom Line! A strong credit report isn’t just about the score—it’s about showing lenders that you’re a reliable, low-risk borrower. Understanding what they truly look for gives you the power to shape your profile and position yourself for better rates, faster approvals, and higher credit limits. Get Expert Help from REI Invest CapitalIf you're ready to clean up your report, raise your score, or get approved for that big loan, REI Invest Capital Loan Credit Repair can help. From removing negative items to adding authorized tradelines, their credit experts create a customized action plan to get results fast. 📞 Call 312-626-0116 today or click here to schedule your free consultation and take the first step toward financial freedom.  Let me take you back to a moment that taught me a very real lesson about credit—specifically, hard inquiries. I remember a few years ago, I was helping a client named Jada, a single mother who had finally stabilized her income and was ready to buy her first home. She was excited, hopeful, and more than ready to walk into that pre-approval meeting with confidence.

But the lender looked at her application and said something that made her stomach drop: “We’d love to approve you, but your score’s too low because of the number of recent credit inquiries. There’s been too much activity.” She was shocked. Jada hadn’t missed any payments, hadn’t maxed out her cards—she’d just been doing what she thought was right: shopping around for the best rates on a car loan, applying for a few credit cards to build her credit history, and prequalifying for a few online store cards. Sound familiar? The truth is, hard inquiries can and do affect your score—but most people don’t understand how they really work. So today, I’m going to walk you through what I explained to Jada that day--the real deal about hard inquiries, how they impact your credit score, how long they stay on your report, and most importantly, how to manage them wisely. 💳 What Is a Hard Inquiry?A hard inquiry (or "hard pull") happens when a lender or creditor checks your credit report because you’ve applied for new credit. This can include:

Unlike a soft inquiry (like checking your own credit or getting prequalified), hard inquiries can affect your score. And lenders use them as a measure of how aggressively you're seeking new credit. 💥 How Hard Inquiries Affect Your Credit Score Now, let’s be clear--one hard inquiry won’t destroy your score. On average, it might cost you 2 to 5 points. But here’s where it gets tricky: multiple inquiries in a short period of time can start to add up—especially if they’re spread across different types of credit (cards, loans, etc.). When I looked at Jada’s report, she had seven hard inquiries in four months. Her score had dropped more than 30 points just from those inquiries alone. And while 30 points might not seem like much, it made the difference between approval and denial. 🧠 The Psychology Behind It Lenders see multiple inquiries as a potential red flag. Why? Because it can make it look like you’re desperate for credit, taking on too much debt too quickly, or struggling financially—even if that’s not the case. And unfortunately, credit scoring models don’t know the “why”—they just see the data. 🕒 How Long Do Hard Inquiries Stay on Your Credit Report? Hard inquiries stay on your report for two years, but the good news is:

So if you’ve got a few dings on your report now, know that time will heal some of the damage—as long as you don’t keep adding more. ✋🏽 When It’s Safe to Rate-Shop (And How to Do It Smart) Here’s something Jada didn’t know—and most people don’t: If you’re shopping for one type of loan, like a mortgage or auto loan, and do it within a short period (typically 14–45 days depending on the scoring model), all those inquiries count as ONE. This is known as a “rate-shopping window.” ✅ Smart Tip: When you’re comparing loan options, gather your quotes in one 2-week window to minimize damage to your score. ⚠️ Where People Go Wrong (Mistakes to Avoid)Here are some of the most common mistakes I see that lead to unnecessary inquiries:

These little habits might seem harmless in the moment, but over time, they chip away at your score and credibility. 🧰 How to Check and Manage Your InquiriesJust like I taught Jada, here’s how you can take control of your hard inquiries right now: 🔍 Step 1: Pull Your ReportsGo to AnnualCreditReport.com and get all three credit reports. Look under the “Inquiries” section to see what’s listed. 📝 Step 2: Verify Each OneIf you don’t recognize an inquiry, it could be a sign of fraud or mistaken identity. Contact the creditor listed or file a dispute. 🧹 Step 3: Limit Future Inquiries

💬 What I Told Jada (And What I’ll Tell You)“Credit is about strategy, not just spending,” I told her. “Inquiries are small, but they add up. You have to play the long game.” We worked together to dispute one unauthorized inquiry, slowed down her credit applications, and added a few positive tradelines to balance things out. Within 60 days, her score recovered—and she got her pre-approval letter. Today, she’s a homeowner. And now? She educates her friends on credit. 📅 Want Me to Review Your Credit Report with You?If you’re unsure how inquiries are affecting your score, or if your report feels like a mystery you can’t crack--let’s go through it together. We offer free 30-minute credit consultations where we’ll:

👉 Book your free consultation here or 📞 Call us today at 312–626–0116 The truth about hard inquiries? They’re not your enemy—but they’re not harmless either. The more you understand them, the more power you have over your credit future. Let’s fix what’s holding you back—and get you closer to that approval you’ve been working for.  Errors on your credit report can be more than just an inconvenience—they can cost you access to loans, better interest rates, apartment approvals, or even employment opportunities. Yet according to the Federal Trade Commission, nearly 20% of consumers have at least one verified error on their credit reports that could negatively impact their score.

That’s why the credit experts at REI Invest Capital Loan Credit Repair are providing this clear, step-by-step guide to help consumers dispute inaccurate information and improve their credit health—starting with the basics. 🧾 Why Credit Report Accuracy MattersYour credit report is a detailed history of how you’ve handled debt. It includes information on credit cards, loans, payment history, collections, and more. Lenders and financial institutions rely on this report to make major decisions—so even one mistake can lead to rejections or higher interest rates. “People often assume their credit report is correct just because it’s from a major bureau,” says a credit specialist at REI Invest Capital Loan Repair. “But that’s not always the case. We've seen clients denied mortgages or business loans over errors they didn’t know existed.” 🔍 Common Credit Report Errors to Watch ForBefore jumping into the dispute process, it’s important to know what to look for. The most common errors REI Invest Capital finds on clients’ reports include:

🛠️ Step-by-Step: How to Dispute Errors on Your Credit ReportHere’s the exact process REI Invest Capital recommends for correcting credit report inaccuracies: Step 1: Pull All Three Credit ReportsVisit AnnualCreditReport.com to access free reports from Experian, Equifax, and TransUnion. Check all three—errors may appear on one report but not the others. Step 2: Identify the InaccuracyReview your reports line by line and highlight anything that looks incorrect, such as:

Step 3: Gather Supporting DocumentationYou’ll need proof to support your dispute. This could include:

Step 4: Submit the Dispute to Each Credit BureauYou can file disputes online, by phone, or by mail. REI Invest Capital strongly recommends filing in writing and including copies of your supporting documents. Addresses for mail disputes:

Step 5: Wait for a Response (Typically 30–45 Days)Under the Fair Credit Reporting Act (FCRA), bureaus must investigate and respond to disputes within 30 days. If the bureau agrees with your dispute, they will update or remove the item. Be sure to request an updated copy of your credit report after the investigation is completed. ⚠️ When to Seek Professional HelpWhile some disputes are straightforward, others are more complex—especially when dealing with identity theft, aggressive collectors, or repeated errors. That’s when working with a credit repair firm like REI Invest Capital Loan Credit Repair can save time, reduce stress, and increase your chances of success. Their team specializes in:

📅 Schedule Your Free 30-Minute Credit Repair ConsultationNot sure where to start? The team at REI Invest Capital offers free, no-obligation credit consultations to review your report, pinpoint errors, and walk you through the dispute process step-by-step. 👉 Click here to book your free consultation: 🗝️ Final ThoughtsYour credit report is too important to ignore. With the right strategy and guidance, you can take control of your financial story, eliminate harmful errors, and start building a stronger credit future. REI Invest Capital Loan Credit Repair is here to help you every step of the way—from identifying the issues to fixing them for good.  For many Americans, a credit score is just a number—until it prevents them from getting a loan, renting an apartment, or launching a business. But what most don’t realize is that the credit score isn’t just about how much you owe or whether you pay on time. It’s shaped by multiple components, each with its own weight and impact on your financial health.

To demystify the credit scoring process, experts at REI Invest Capital Loan Credit Repair, a nationwide credit consulting firm, have broken down each element of your credit report--line by line—to uncover what’s really dragging your score down, and how you can take action. 📊 Understanding the Credit Score FormulaCredit scores, typically ranging from 300 to 850, are calculated using formulas developed by companies like FICO and VantageScore. While the exact formulas are proprietary, the five core categories used to evaluate your score are widely known: Factor Weight in Score: Payment History 35% Credit Utilization 30% Length of Credit History 15% New Credit/Inquiries 10% Credit Mix 10% Let’s break down each one—and identify the common pitfalls that might be silently damaging your credit. 🧾 1. Payment History (35%)What It Includes:

What’s Hurting You:

How to Fix It:

💳 2. Credit Utilization (30%)What It Includes:

What’s Hurting You:

How to Fix It:

🕰️ 3. Length of Credit History (15%)What It Includes:

What’s Hurting You:

How to Fix It:

📝 4. New Credit & Inquiries (10%)What It Includes:

How to Fix It:

🧠 5. Credit Mix (10%)What It Includes:

How to Fix It:

🛠️ Bonus: Common Reporting Errors That Artificially Hurt ScoresIn addition to structural issues, credit report errors also play a major role in score suppression. REI Invest Capital has helped thousands of clients uncover and resolve hidden mistakes such as:

These errors can be disputed and removed, often leading to dramatic score improvements in as little as 30–60 days. 🗓️ Need Help Fixing What’s Hurting Your Credit?Understanding your credit is only half the battle--taking action is what leads to results. That’s where REI Invest Capital Loan Credit Repair comes in. Their team of credit experts offers:

📅 Schedule your FREE 30-minute Credit Repair Consultation today: 👉 https://calendly.com/publicitybrandpr/credit-repair-consultation?share_attribution=expiring_link 🔑 Final Thoughts: Your Credit Score Is a Tool—Learn How to Use ItYour credit score isn’t just a number—it’s a reflection of how well you understand and manage your financial reputation. By learning what each section of your report really means, and knowing how to fix the issues dragging you down, you can take back control of your financial life. With expert help from REI Invest Capital Loan Credit Repair, you don’t have to navigate it alone. Credit Report vs. Credit Score: What’s the Difference and Why It Matters as an Entrepreneur3/6/2025

As an entrepreneur, I’ve learned this one lesson the hard way: your personal and business credit are silent partners in your success. Whether you’re applying for funding, leasing an office space, or setting up vendor accounts, your financial profile is always working behind the scenes—either for you or against you.

Yet one of the most common questions I get from new (and even seasoned) business owners is: “What’s the difference between my credit report and my credit score? Aren’t they the same thing?” Nope. Not even close. And if you don’t understand the difference, you might miss major opportunities—or worse, make decisions that hurt your financial future. Let’s break it down the way I explain it to clients inside REI Invest Capital. 📊 Your Credit Score: The 3-Digit SnapshotYour credit score is like your GPA—it’s a number that summarizes your creditworthiness at a glance. Most lenders use FICO® scores, which range from 300 to 850, though there are other scoring models (like VantageScore). This score is calculated based on five key components:

✅ Why it matters as an entrepreneur:If you plan to:

Then your personal credit score is often the first thing underwriters check—especially if you’re a startup or sole proprietor without a strong business credit file. Even if your business has its own EIN and LLC, if your credit score is too low, you could still get denied or pay higher interest rates. 📄 Your Credit Report: The Full StoryYour credit report is the actual document that shows what’s behind the score. It includes detailed data like:

That one collection might only drop your score by a few points, but a manual underwriter (like at a bank or SBA lender) will see the report and may deny your application based on what they read—not just the score. “Your report tells the story. Your score is just the summary.” 🔍 Real-Life Example: Meet Carlos, a Startup OwnerCarlos came to us at REI Invest Capital with a solid business plan and a 715 credit score. He wanted to apply for a $50,000 business line of credit to launch his e-commerce fulfillment company. He was confident—until he got declined. Twice. When we reviewed his credit report, we discovered:

Even though his score was good, his report told a riskier story. ✅ What we did:

Result? His report looked stronger, his utilization dropped, and he got approved at a better interest rate--all without changing his score by more than 10 points. 💡 Key Takeaways for Entrepreneurs

📞 Let’s Review Your Credit Report TogetherIf you’re an entrepreneur preparing for funding, expansion, or just trying to build smart, don’t go into it blind. At REI Invest Capital Loan Credit Repair, we help business owners:

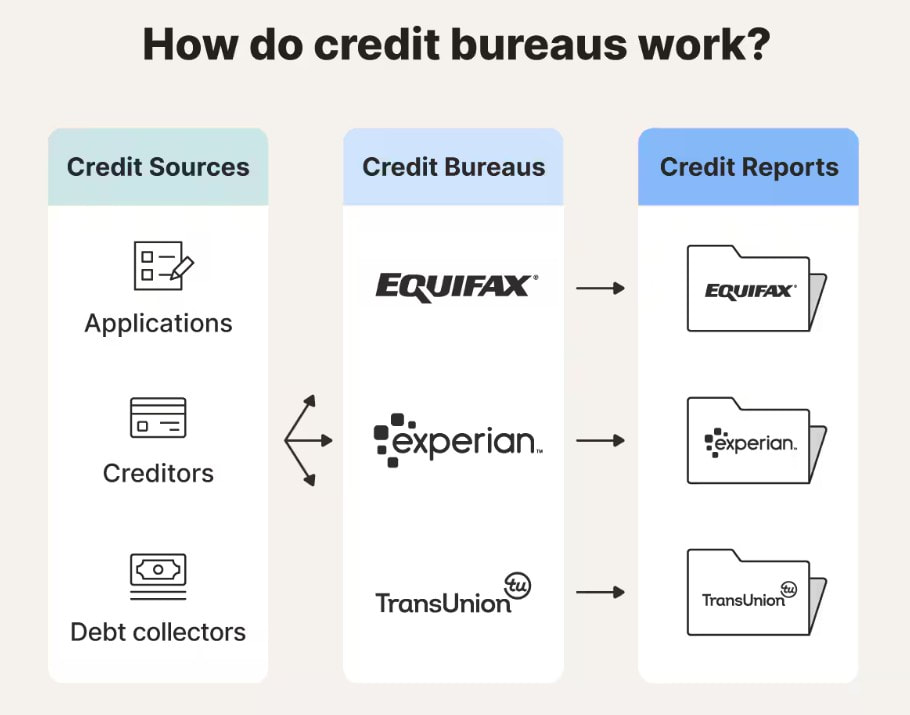

📅 Book your FREE 30-minute consultation today 📞 Or call us directly at (312) 626-0116 Bottom Line: Your credit report and credit score are both powerful tools--but they are not the same thing. Understanding both is not just smart... it's essential for any entrepreneur building a business that lasts.  When it comes to credit, many consumers focus solely on their credit score—but behind every score is a credit report, and behind every report are the three major credit bureaus: Experian, Equifax, and TransUnion. Each of these agencies plays a vital role in how lenders, landlords, employers, and insurers view your financial trustworthiness. But here’s what most people don’t realize: not all credit reports are the same—and the bureaus don’t always agree. To help consumers, business owners, and aspiring homeowners understand the full picture, REI Invest Capital Loan Credit Repair has created this comprehensive guide to explain how each bureau works, how they differ, and why it’s crucial to monitor all three. 📊 What Are the 3 Major Credit Bureaus? The three credit reporting agencies—Experian, Equifax, and TransUnion—are private companies that collect, store, and manage your credit data. They each maintain individual credit files for every consumer, based on information provided by lenders, creditors, utility companies, and public records. These credit bureaus are not government entities, but they are regulated under the Fair Credit Reporting Act (FCRA) to ensure accuracy and protect consumer rights. 🔁 How the Credit Bureaus Work - Although they’re often viewed as a unified system, the credit bureaus are independent organizations with unique business models, algorithms, and data relationships. Here's how they operate: 🔹 1. Data Collection - Credit bureaus do not create your credit activity—they simply collect data reported by creditors, lenders, public agencies, and third-party data providers. Each time you make a payment, miss one, open a credit card, apply for a loan, or default on a bill, the entity managing that account may report the activity to one, two, or all three bureaus. However, reporting is voluntary, and not every lender reports to every bureau. This is why each report may contain slightly different information, even though they’re all tracking the same consumer. 🔹 2. Credit File Compilation - Once the bureaus receive data, they organize it into your individual credit file, linked to identifiers like your:

🔹 3. Scoring Model Application - Credit bureaus apply scoring models—most commonly FICO® or VantageScore—to your file. These models assess how risky you appear based on your:

For example:

🔹 4. Credit File Sales to Third Parties - Credit bureaus sell access to your credit report and score to:

This is also why it’s essential to monitor your reports regularly—errors or outdated items can cost you opportunities you never even knew you lost. 🏛️ The Three Bureaus at a Glance Experian

❗ Why the Bureaus Don’t Always Match - Consumers are often surprised to learn that their credit reports—and even their scores--can differ from bureau to bureau. Here’s why: 1. Not All Lenders Report to All Three BureausSome creditors only report to one or two bureaus. For example, a regional credit union may only report to Equifax, leaving Experian and TransUnion in the dark. 2. Different Scoring Models and VersionsEach bureau may use a different version of FICO or VantageScore, and scoring criteria can vary. That’s why your TransUnion score might show 715, while your Experian score says 690. 3. Update Timing and FrequencyData may be reported at different times to each bureau. A payment made today might appear on Experian this week, but not on Equifax for another 10 days. 4. Errors and File MismatchesMisspelled names, outdated addresses, or mixed-up Social Security numbers can lead to incorrect information being included—or excluded—from your file. REI Invest Capital frequently corrects these types of issues through targeted dispute strategies. 📋 Why You Must Check All Three Credit Reports - Checking one report gives you part of the picture. Checking all three gives you the full story. REI Invest Capital strongly encourages clients to:

🔧 How REI Invest Capital Helps As a leader in personal and business credit improvement, REI Invest Capital Loan Credit Repair assists clients with: ✅ Full three-bureau credit report analysis ✅ Disputes and removal of inaccurate or harmful items ✅ Authorized tradeline programs to strengthen credit files ✅ Rapid rescore strategies for time-sensitive approvals ✅ Personalized education and support for rebuilding credit confidence Whether you're applying for a home, building your business, or repairing damage from the past, understanding what’s on each report—and how it affects your creditworthiness—is the first step. 📞 Need a Credit Report Review? REI Invest Capital, Can Help If you’re unsure what’s on your credit reports—or if you’ve only ever looked at one—REI Invest Capital can help you review, compare, and take action. 📅 Schedule your free 30-minute consultation: 📞 Or call us at (312) 626-0116 🧠 Final Word Your credit score is important—but it’s only as accurate as the data behind it. And that data lives in three different places. By understanding the role each credit bureau plays, how they work, and how to manage all three reports, you gain the clarity and confidence to build a financial future on solid ground.  Your credit report is one of the most powerful financial tools you have—yet for many people, it's also one of the most misunderstood. Whether you’re applying for a mortgage, starting a business, getting a new credit card, or simply aiming for better financial health, your credit report plays a major role. In this comprehensive guide, we break down everything you need to know about credit reports: what they are, how they work, how they affect you, and most importantly, how to manage and protect them.

1. What Is a Credit Report? A credit report is a detailed record of your credit history, compiled by credit bureaus based on information provided by lenders and public records. It includes your payment history, credit accounts, outstanding balances, and more. Lenders, landlords, insurance companies, and sometimes employers use it to assess your financial responsibility. 2. The Difference Between Credit Report and Credit Score - A credit report is the raw data—a detailed list of your credit history. Your credit score is a three-digit number (usually ranging from 300 to 850) calculated based on the information in your credit report. The score summarizes your creditworthiness. 3. Who Creates and Maintains Credit Reports? The three major credit bureaus in the U.S. are:

4. What Information Is in a Credit Report? Your credit report contains:

5. How to Access Your Credit Report - Federal law allows you to access a free credit report from each bureau once every 12 months at AnnualCreditReport.com. During crises like COVID-19, the bureaus may offer reports more frequently. 6. Why Your Credit Report Matters Your credit report impacts:

7. How to Read and Understand Your Credit Report Look for:

8. Common Credit Report Errors - Some of the most common errors include:

9. How to Dispute Errors on Your Credit Report - Steps to dispute:Get your report from all three bureaus

10. The Role of Hard and Soft Inquiries

11. How Long Information Stays on Your Report

12. Tips to Build and Maintain a Healthy Credit Report

13. How to Freeze or Lock Your Credit Report - Freezing your credit restricts access to your report, protecting you from fraud. You can request a freeze through each bureau’s website. 14. How Credit Reports Affect Loans, Jobs, and Insurance - Lenders use your report to assess risk. Employers may review it for job-related responsibilities. Insurers may factor it into premium pricing. 15. Protecting Your Identity and Credit

16. Special Tips for Business Owners - Business owners must manage both personal and business credit. Use business credit accounts responsibly, establish a D-U-N-S number, and monitor your business credit with Dun & Bradstreet, Experian Business, and Equifax Business. 17. Credit Repair Myths and Facts Myth: Credit repair companies can remove accurate negative items. Fact: Only incorrect or outdated information can be removed. Myth: Closing credit cards improves your score. Fact: It may actually hurt by lowering your total available credit. Myth: Paying off collections removes them from your report. Fact: They remain but may be marked as paid. 18. Resources and Tools to Monitor Your Credit

Understanding your credit report is the first step to financial empowerment. With the right knowledge, you can take control of your credit, correct errors, and make informed financial decisions. Whether you're a student, employee, or business owner, your credit report is your financial fingerprint. Ready to take control of your financial future? Start by downloading your free credit reports today and reviewing them carefully. If you need help disputing errors, boosting your score, or growing your credit strategically, REI Invest Capital Loan Credit Repair is here to guide you every step of the way. Click here to schedule your free consultation or call 312-626-0116 and let us help you build, protect, and leverage your credit the smart way. Your future is too important to leave to chance. |

RSS Feed

RSS Feed

REI Invest Capital

401 N. Michigan Ave.

Chicago, IL 60611

Office: 312-626-0116

Schedule Calendly HERE

401 N. Michigan Ave.

Chicago, IL 60611

Office: 312-626-0116

Schedule Calendly HERE

Our Services

Understanding Your Credit

Funding

FAQ

Contact us

Understanding Your Credit

Funding

FAQ

Contact us

© 2024 REI Invest Capital - Loan Credit Repair