Errors on your credit report can be more than just an inconvenience—they can cost you access to loans, better interest rates, apartment approvals, or even employment opportunities. Yet according to the Federal Trade Commission, nearly 20% of consumers have at least one verified error on their credit reports that could negatively impact their score.

That’s why the credit experts at REI Invest Capital Loan Credit Repair are providing this clear, step-by-step guide to help consumers dispute inaccurate information and improve their credit health—starting with the basics. 🧾 Why Credit Report Accuracy MattersYour credit report is a detailed history of how you’ve handled debt. It includes information on credit cards, loans, payment history, collections, and more. Lenders and financial institutions rely on this report to make major decisions—so even one mistake can lead to rejections or higher interest rates. “People often assume their credit report is correct just because it’s from a major bureau,” says a credit specialist at REI Invest Capital Loan Repair. “But that’s not always the case. We've seen clients denied mortgages or business loans over errors they didn’t know existed.” 🔍 Common Credit Report Errors to Watch ForBefore jumping into the dispute process, it’s important to know what to look for. The most common errors REI Invest Capital finds on clients’ reports include:

🛠️ Step-by-Step: How to Dispute Errors on Your Credit ReportHere’s the exact process REI Invest Capital recommends for correcting credit report inaccuracies: Step 1: Pull All Three Credit ReportsVisit AnnualCreditReport.com to access free reports from Experian, Equifax, and TransUnion. Check all three—errors may appear on one report but not the others. Step 2: Identify the InaccuracyReview your reports line by line and highlight anything that looks incorrect, such as:

Step 3: Gather Supporting DocumentationYou’ll need proof to support your dispute. This could include:

Step 4: Submit the Dispute to Each Credit BureauYou can file disputes online, by phone, or by mail. REI Invest Capital strongly recommends filing in writing and including copies of your supporting documents. Addresses for mail disputes:

Step 5: Wait for a Response (Typically 30–45 Days)Under the Fair Credit Reporting Act (FCRA), bureaus must investigate and respond to disputes within 30 days. If the bureau agrees with your dispute, they will update or remove the item. Be sure to request an updated copy of your credit report after the investigation is completed. ⚠️ When to Seek Professional HelpWhile some disputes are straightforward, others are more complex—especially when dealing with identity theft, aggressive collectors, or repeated errors. That’s when working with a credit repair firm like REI Invest Capital Loan Credit Repair can save time, reduce stress, and increase your chances of success. Their team specializes in:

📅 Schedule Your Free 30-Minute Credit Repair ConsultationNot sure where to start? The team at REI Invest Capital offers free, no-obligation credit consultations to review your report, pinpoint errors, and walk you through the dispute process step-by-step. 👉 Click here to book your free consultation: 🗝️ Final ThoughtsYour credit report is too important to ignore. With the right strategy and guidance, you can take control of your financial story, eliminate harmful errors, and start building a stronger credit future. REI Invest Capital Loan Credit Repair is here to help you every step of the way—from identifying the issues to fixing them for good.  For many Americans, a credit score is just a number—until it prevents them from getting a loan, renting an apartment, or launching a business. But what most don’t realize is that the credit score isn’t just about how much you owe or whether you pay on time. It’s shaped by multiple components, each with its own weight and impact on your financial health.

To demystify the credit scoring process, experts at REI Invest Capital Loan Credit Repair, a nationwide credit consulting firm, have broken down each element of your credit report--line by line—to uncover what’s really dragging your score down, and how you can take action. 📊 Understanding the Credit Score FormulaCredit scores, typically ranging from 300 to 850, are calculated using formulas developed by companies like FICO and VantageScore. While the exact formulas are proprietary, the five core categories used to evaluate your score are widely known: Factor Weight in Score: Payment History 35% Credit Utilization 30% Length of Credit History 15% New Credit/Inquiries 10% Credit Mix 10% Let’s break down each one—and identify the common pitfalls that might be silently damaging your credit. 🧾 1. Payment History (35%)What It Includes:

What’s Hurting You:

How to Fix It:

💳 2. Credit Utilization (30%)What It Includes:

What’s Hurting You:

How to Fix It:

🕰️ 3. Length of Credit History (15%)What It Includes:

What’s Hurting You:

How to Fix It:

📝 4. New Credit & Inquiries (10%)What It Includes:

How to Fix It:

🧠 5. Credit Mix (10%)What It Includes:

How to Fix It:

🛠️ Bonus: Common Reporting Errors That Artificially Hurt ScoresIn addition to structural issues, credit report errors also play a major role in score suppression. REI Invest Capital has helped thousands of clients uncover and resolve hidden mistakes such as:

These errors can be disputed and removed, often leading to dramatic score improvements in as little as 30–60 days. 🗓️ Need Help Fixing What’s Hurting Your Credit?Understanding your credit is only half the battle--taking action is what leads to results. That’s where REI Invest Capital Loan Credit Repair comes in. Their team of credit experts offers:

📅 Schedule your FREE 30-minute Credit Repair Consultation today: 👉 https://calendly.com/publicitybrandpr/credit-repair-consultation?share_attribution=expiring_link 🔑 Final Thoughts: Your Credit Score Is a Tool—Learn How to Use ItYour credit score isn’t just a number—it’s a reflection of how well you understand and manage your financial reputation. By learning what each section of your report really means, and knowing how to fix the issues dragging you down, you can take back control of your financial life. With expert help from REI Invest Capital Loan Credit Repair, you don’t have to navigate it alone.  When it comes to rebuilding credit, one of the most common questions people ask is:

“How long do negative items stay on my credit report?” For many, the assumption is that once a debt is paid or settled, it disappears from the report. Unfortunately, that’s far from the truth. According to the credit specialists at REI Invest Capital Loan Credit Repair, the lifespan of negative information can vary based on the type of item, how it's reported, and whether or not it’s disputed or corrected. To help consumers better understand how long these negative marks can impact their credit—and what they can do about it—REI Invest Capital shares insights, timelines, and a real-life story of one woman’s journey from damaged credit to homeownership. 📘 Case Study: Jasmine's Path to Homeownership—Delayed by a Dormant CollectionJasmine, a 36-year-old graphic designer from Chicago, had done everything right for the past two years. She had paid her credit cards on time, avoided unnecessary debt, and kept her balances low. When she applied for a pre-approval to buy her first condo, she expected smooth sailing. But she was denied. After reviewing her credit report with an advisor from REI Invest Capital Loan Credit Repair, Jasmine was shocked to find an old $412 medical collection from four years ago—one she thought had been resolved through insurance. It had been quietly hurting her score for years and was never disputed. “I didn’t even know it was there,” she said. “No one ever contacted me—and it never showed up in my credit monitoring app.” Her story is not uncommon. Many consumers are unaware that negative items—even small ones—can linger for years and impact major financial decisions. 📊 Types of Negative Items and How Long They Stay on Your Credit ReportREI Invest Capital breaks down the most common negative items and their official reporting lifespans according to the Fair Credit Reporting Act (FCRA): 1. Late PaymentsTime on Report: 7 years from the date of the missed payment A single late payment (30+ days past due) can hurt your score by 60–100 points, especially if your history is otherwise clean. Even if you bring the account current, it will still remain on your report for seven years from the original delinquency date. 2. Collection Accounts Time on Report: 7 years from the date of the first delinquency on the original account Whether paid or unpaid, a collection stays for seven years. However, REI Invest Capital often helps clients negotiate pay-for-delete agreements with collection agencies or disputes items that are reporting inaccurately. 3. Charge-OffsTime on Report: 7 years from the date of the first missed payment that led to the charge-off A charge-off occurs when a creditor deems the debt uncollectible. Even if you later pay it off, it remains a negative mark unless the creditor agrees to remove it. 4. Bankruptcies

5. ForeclosuresTime on Report: 7 years from the foreclosure date Foreclosures have a significant impact on a consumer's credit score but lose weight over time. After year two or three, the impact starts to lessen if positive credit behavior follows. 6. RepossessionsTime on Report: 7 years from the date of the first missed payment Voluntary or involuntary repossessions both appear on reports and can reduce a score by over 100 points. 7. Civil Judgments and Tax Liens (No Longer Reported) As of recent changes in credit reporting practices, civil judgments and tax liens no longer appear on credit reports, thanks to settlements with credit bureaus and regulators. However, unpaid debts related to judgments may still be collected and affect your ability to secure credit. 🧠 The Misconception About “Paying It Off ”Many people believe that once a negative account is paid or settled, it will be removed. But unless the creditor agrees to delete the account, the item remains visible for the full reporting period. What changes is the status—from “unpaid” to “paid”—which may improve how lenders view it, but the impact on your score can still linger. That’s why REI Invest Capital works with clients to not just resolve debts, but also to negotiate deletions, correct inaccuracies, and add positive tradelines to offset the damage. 🧰 How REI Invest Capital Helps Shorten the Impact While the law sets timelines, credit repair professionals can help clients take proactive steps:

If you’re unsure what negative items are on your credit report—or how long they’ve been affecting your score--REI Invest Capital Loan Credit Repair can help. 📅 Schedule your free 30-minute consultation:📞 Or call (312) 626-0116 to speak directly with a credit specialist. 💬 Final Word Negative items don’t have to define your credit story—but ignoring them can delay your dreams. Knowing how long they last and how to address them puts the power back in your hands. With expert help from REI Invest Capital Loan Credit Repair, clients like Jasmine don’t just wait for credit to “get better”—they take charge of the process and write a new chapter. Credit Report vs. Credit Score: What’s the Difference and Why It Matters as an Entrepreneur3/6/2025

As an entrepreneur, I’ve learned this one lesson the hard way: your personal and business credit are silent partners in your success. Whether you’re applying for funding, leasing an office space, or setting up vendor accounts, your financial profile is always working behind the scenes—either for you or against you.

Yet one of the most common questions I get from new (and even seasoned) business owners is: “What’s the difference between my credit report and my credit score? Aren’t they the same thing?” Nope. Not even close. And if you don’t understand the difference, you might miss major opportunities—or worse, make decisions that hurt your financial future. Let’s break it down the way I explain it to clients inside REI Invest Capital. 📊 Your Credit Score: The 3-Digit SnapshotYour credit score is like your GPA—it’s a number that summarizes your creditworthiness at a glance. Most lenders use FICO® scores, which range from 300 to 850, though there are other scoring models (like VantageScore). This score is calculated based on five key components:

✅ Why it matters as an entrepreneur:If you plan to:

Then your personal credit score is often the first thing underwriters check—especially if you’re a startup or sole proprietor without a strong business credit file. Even if your business has its own EIN and LLC, if your credit score is too low, you could still get denied or pay higher interest rates. 📄 Your Credit Report: The Full StoryYour credit report is the actual document that shows what’s behind the score. It includes detailed data like:

That one collection might only drop your score by a few points, but a manual underwriter (like at a bank or SBA lender) will see the report and may deny your application based on what they read—not just the score. “Your report tells the story. Your score is just the summary.” 🔍 Real-Life Example: Meet Carlos, a Startup OwnerCarlos came to us at REI Invest Capital with a solid business plan and a 715 credit score. He wanted to apply for a $50,000 business line of credit to launch his e-commerce fulfillment company. He was confident—until he got declined. Twice. When we reviewed his credit report, we discovered:

Even though his score was good, his report told a riskier story. ✅ What we did:

Result? His report looked stronger, his utilization dropped, and he got approved at a better interest rate--all without changing his score by more than 10 points. 💡 Key Takeaways for Entrepreneurs

📞 Let’s Review Your Credit Report TogetherIf you’re an entrepreneur preparing for funding, expansion, or just trying to build smart, don’t go into it blind. At REI Invest Capital Loan Credit Repair, we help business owners:

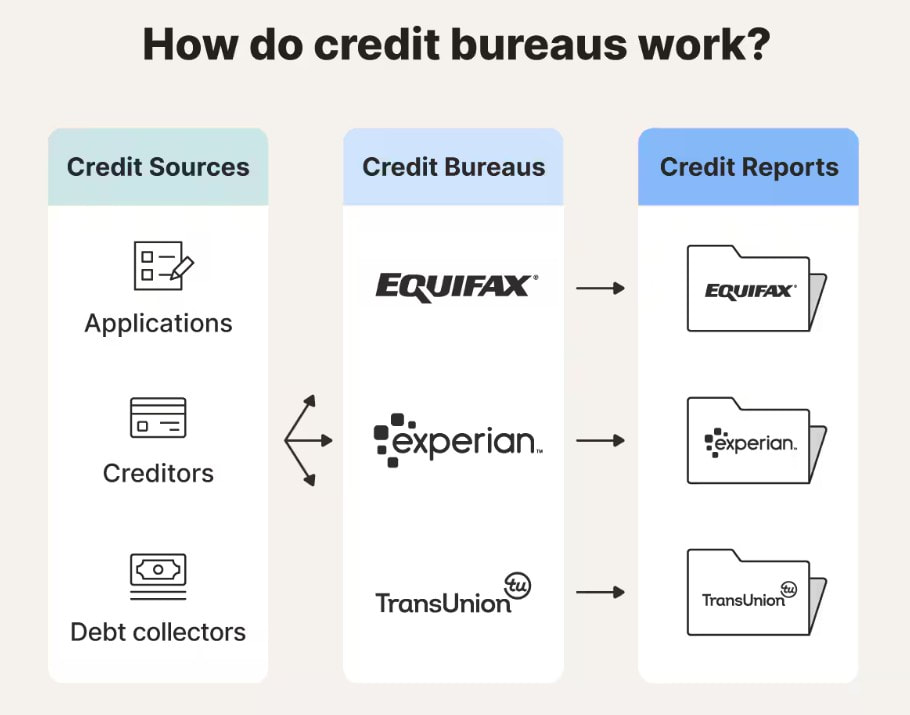

📅 Book your FREE 30-minute consultation today 📞 Or call us directly at (312) 626-0116 Bottom Line: Your credit report and credit score are both powerful tools--but they are not the same thing. Understanding both is not just smart... it's essential for any entrepreneur building a business that lasts.  When it comes to credit, many consumers focus solely on their credit score—but behind every score is a credit report, and behind every report are the three major credit bureaus: Experian, Equifax, and TransUnion. Each of these agencies plays a vital role in how lenders, landlords, employers, and insurers view your financial trustworthiness. But here’s what most people don’t realize: not all credit reports are the same—and the bureaus don’t always agree. To help consumers, business owners, and aspiring homeowners understand the full picture, REI Invest Capital Loan Credit Repair has created this comprehensive guide to explain how each bureau works, how they differ, and why it’s crucial to monitor all three. 📊 What Are the 3 Major Credit Bureaus? The three credit reporting agencies—Experian, Equifax, and TransUnion—are private companies that collect, store, and manage your credit data. They each maintain individual credit files for every consumer, based on information provided by lenders, creditors, utility companies, and public records. These credit bureaus are not government entities, but they are regulated under the Fair Credit Reporting Act (FCRA) to ensure accuracy and protect consumer rights. 🔁 How the Credit Bureaus Work - Although they’re often viewed as a unified system, the credit bureaus are independent organizations with unique business models, algorithms, and data relationships. Here's how they operate: 🔹 1. Data Collection - Credit bureaus do not create your credit activity—they simply collect data reported by creditors, lenders, public agencies, and third-party data providers. Each time you make a payment, miss one, open a credit card, apply for a loan, or default on a bill, the entity managing that account may report the activity to one, two, or all three bureaus. However, reporting is voluntary, and not every lender reports to every bureau. This is why each report may contain slightly different information, even though they’re all tracking the same consumer. 🔹 2. Credit File Compilation - Once the bureaus receive data, they organize it into your individual credit file, linked to identifiers like your:

🔹 3. Scoring Model Application - Credit bureaus apply scoring models—most commonly FICO® or VantageScore—to your file. These models assess how risky you appear based on your:

For example:

🔹 4. Credit File Sales to Third Parties - Credit bureaus sell access to your credit report and score to:

This is also why it’s essential to monitor your reports regularly—errors or outdated items can cost you opportunities you never even knew you lost. 🏛️ The Three Bureaus at a Glance Experian

❗ Why the Bureaus Don’t Always Match - Consumers are often surprised to learn that their credit reports—and even their scores--can differ from bureau to bureau. Here’s why: 1. Not All Lenders Report to All Three BureausSome creditors only report to one or two bureaus. For example, a regional credit union may only report to Equifax, leaving Experian and TransUnion in the dark. 2. Different Scoring Models and VersionsEach bureau may use a different version of FICO or VantageScore, and scoring criteria can vary. That’s why your TransUnion score might show 715, while your Experian score says 690. 3. Update Timing and FrequencyData may be reported at different times to each bureau. A payment made today might appear on Experian this week, but not on Equifax for another 10 days. 4. Errors and File MismatchesMisspelled names, outdated addresses, or mixed-up Social Security numbers can lead to incorrect information being included—or excluded—from your file. REI Invest Capital frequently corrects these types of issues through targeted dispute strategies. 📋 Why You Must Check All Three Credit Reports - Checking one report gives you part of the picture. Checking all three gives you the full story. REI Invest Capital strongly encourages clients to:

🔧 How REI Invest Capital Helps As a leader in personal and business credit improvement, REI Invest Capital Loan Credit Repair assists clients with: ✅ Full three-bureau credit report analysis ✅ Disputes and removal of inaccurate or harmful items ✅ Authorized tradeline programs to strengthen credit files ✅ Rapid rescore strategies for time-sensitive approvals ✅ Personalized education and support for rebuilding credit confidence Whether you're applying for a home, building your business, or repairing damage from the past, understanding what’s on each report—and how it affects your creditworthiness—is the first step. 📞 Need a Credit Report Review? REI Invest Capital, Can Help If you’re unsure what’s on your credit reports—or if you’ve only ever looked at one—REI Invest Capital can help you review, compare, and take action. 📅 Schedule your free 30-minute consultation: 📞 Or call us at (312) 626-0116 🧠 Final Word Your credit score is important—but it’s only as accurate as the data behind it. And that data lives in three different places. By understanding the role each credit bureau plays, how they work, and how to manage all three reports, you gain the clarity and confidence to build a financial future on solid ground.  Your credit report is one of the most powerful financial tools you have—yet for many people, it's also one of the most misunderstood. Whether you’re applying for a mortgage, starting a business, getting a new credit card, or simply aiming for better financial health, your credit report plays a major role. In this comprehensive guide, we break down everything you need to know about credit reports: what they are, how they work, how they affect you, and most importantly, how to manage and protect them.

1. What Is a Credit Report? A credit report is a detailed record of your credit history, compiled by credit bureaus based on information provided by lenders and public records. It includes your payment history, credit accounts, outstanding balances, and more. Lenders, landlords, insurance companies, and sometimes employers use it to assess your financial responsibility. 2. The Difference Between Credit Report and Credit Score - A credit report is the raw data—a detailed list of your credit history. Your credit score is a three-digit number (usually ranging from 300 to 850) calculated based on the information in your credit report. The score summarizes your creditworthiness. 3. Who Creates and Maintains Credit Reports? The three major credit bureaus in the U.S. are:

4. What Information Is in a Credit Report? Your credit report contains:

5. How to Access Your Credit Report - Federal law allows you to access a free credit report from each bureau once every 12 months at AnnualCreditReport.com. During crises like COVID-19, the bureaus may offer reports more frequently. 6. Why Your Credit Report Matters Your credit report impacts:

7. How to Read and Understand Your Credit Report Look for:

8. Common Credit Report Errors - Some of the most common errors include:

9. How to Dispute Errors on Your Credit Report - Steps to dispute:Get your report from all three bureaus

10. The Role of Hard and Soft Inquiries

11. How Long Information Stays on Your Report

12. Tips to Build and Maintain a Healthy Credit Report

13. How to Freeze or Lock Your Credit Report - Freezing your credit restricts access to your report, protecting you from fraud. You can request a freeze through each bureau’s website. 14. How Credit Reports Affect Loans, Jobs, and Insurance - Lenders use your report to assess risk. Employers may review it for job-related responsibilities. Insurers may factor it into premium pricing. 15. Protecting Your Identity and Credit

16. Special Tips for Business Owners - Business owners must manage both personal and business credit. Use business credit accounts responsibly, establish a D-U-N-S number, and monitor your business credit with Dun & Bradstreet, Experian Business, and Equifax Business. 17. Credit Repair Myths and Facts Myth: Credit repair companies can remove accurate negative items. Fact: Only incorrect or outdated information can be removed. Myth: Closing credit cards improves your score. Fact: It may actually hurt by lowering your total available credit. Myth: Paying off collections removes them from your report. Fact: They remain but may be marked as paid. 18. Resources and Tools to Monitor Your Credit

Understanding your credit report is the first step to financial empowerment. With the right knowledge, you can take control of your credit, correct errors, and make informed financial decisions. Whether you're a student, employee, or business owner, your credit report is your financial fingerprint. Ready to take control of your financial future? Start by downloading your free credit reports today and reviewing them carefully. If you need help disputing errors, boosting your score, or growing your credit strategically, REI Invest Capital Loan Credit Repair is here to guide you every step of the way. Click here to schedule your free consultation or call 312-626-0116 and let us help you build, protect, and leverage your credit the smart way. Your future is too important to leave to chance. |

RSS Feed

RSS Feed

REI Invest Capital

401 N. Michigan Ave.

Chicago, IL 60611

Office: 312-626-0116

Schedule Calendly HERE

401 N. Michigan Ave.

Chicago, IL 60611

Office: 312-626-0116

Schedule Calendly HERE

Our Services

Understanding Your Credit

Funding

FAQ

Contact us

Understanding Your Credit

Funding

FAQ

Contact us

© 2024 REI Invest Capital - Loan Credit Repair